Office Address

123/A, Miranda City Likaoli Prikano, Dope

Phone Number

+0989 7876 9865 9

+(090) 8765 86543 85

Email Address

info@example.com

example.mail@hum.com

123/A, Miranda City Likaoli Prikano, Dope

+0989 7876 9865 9

+(090) 8765 86543 85

info@example.com

example.mail@hum.com

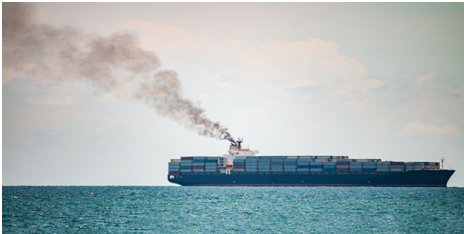

The Saudi Arabian hub port of Jeddah is reporting a

two-thirds drop in calls from the top ten carriers, as re-routing vessels on Asia-European routes add

5,800 nautical miles to the journey of each container, pushing up CO2

emissions. Calls at Jeddah by the top carriers were down 67%, with the port now

handling shuttle services plying the Suez Canal that need not venture far into the

Red Sea, or through the Bab-el-Mandeb strait.

Vessel sizes now

average 5,600 teu, versus the pre-Red Sea crisis average of 8,625 teu,

according to Alphaliner data.

The case of MSC is

particularly stark, its vessel calls at Jeddah dropping from 230 in Q1 23 to

around 60 in the first quarter of this year.

Hoping to make up for

the service shortfall, MSC has added calls at Jeddah and King Abdullah on its

Levante Express service, and the 9,200 teu MSC Maria Elena is

scheduled for an inaugural call at King Abdullah port on Sunday.

Meanwhile, according

to Xeneta’s CO2 per-tonne-km measure, the carbon emissions index (CEI), the Far

East-Mediterranean trade, which in Q3 23 was one of the best performers in

terms of emissions, became the worst in

the first quarter of this year, with a CEI score of 140.8 – an increase of over

60%.

The CEI index for Far

East-Northern Europe trades also increased in the first quarter, to 111, a 20%

jump year on year. However, Xeneta analyst Emily Stausbøll noted that the

increased distance on this trade was partially mitigated by an improved vessel

filling factor, up 6.1%.

Although overcapacity was one of container

shipping’s biggest concerns last autumn, Xeneta’s data appears to demonstrate

that Red Sea diversions have completely taken up this slack.

The global average

speed of 12,000-17,000 teu ships rose to 15.4 knots in January, and has stayed

above 15 knots since. But not only are vessels sailing faster; but older,

smaller and less fuel-efficient vessels are being redeployed.

“Even if we see an

improvement in Q2 from Q1, if ships are

continuing to sail longer distances around the Cape of Good Hope, then it is

almost inevitable that the CEI performance will be worse when compared with

2023 levels,” wrote Ms Stausbøll.

“Regardless, the

deterioration in the CEI in Q1 24 demonstrates the severe and immediate impact

conflict has on supply chain carbon emissions,” she added.

Meanwhile, the

propensity for some shippers to switch to air cargo or sea-air routings through

Dubai or Colombo have raised emission levels further