Office Address

123/A, Miranda City Likaoli Prikano, Dope

Phone Number

+0989 7876 9865 9

+(090) 8765 86543 85

Email Address

info@example.com

example.mail@hum.com

123/A, Miranda City Likaoli Prikano, Dope

+0989 7876 9865 9

+(090) 8765 86543 85

info@example.com

example.mail@hum.com

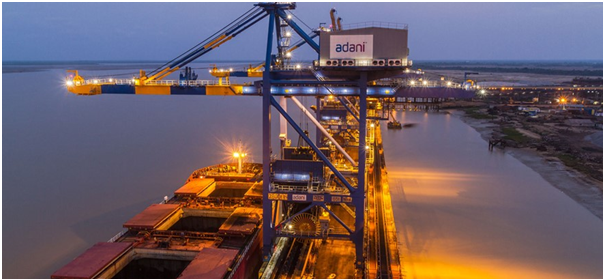

The

company’s monthly cargo run rate, reaching approximately 35 MMT, suggests a

strong likelihood of surpassing its revised guidance of 400 MMT for FY24,

brokerage firm Motilal Oswal said in a note.

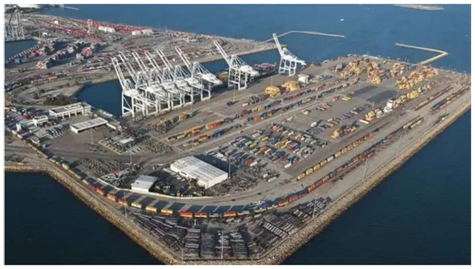

With a robust logistics business, APSEZ saw a 21 per

cent year-on-year increase in rail volume in FY24. Its extensive pan-India

presence, coupled with strong pricing power and a major proportion of sticky

cargo, contributes to its consistent market share gains.

The company’s investment in infrastructure for its

logistics business is expected to enhance longterm cash flows and earnings.

With a net debt-to-EBITDA ratio of 2.5 times as of December 2023, APSEZ

maintains a favourable leverage position. EBITDA is earnings before interest,

taxes, depreciation and amortisation.

The

port operator anticipates major growth in the logistics sector, highlighted by

its achievement of the highest quarterly rail volume and expansion in

warehousing capacity. Furthermore, the

addition of rakes and expansion plans signify its commitment to future growth

in the logistics segment, the Mumbai-based brokerage highlighted.

Despite the potential impact of the Red Sea crisis on its

traffic, currently constituting approximately 10 per cent of its total volume,

APSEZ remains resilient. However, continued

disruption could affect volumes in the long term.

Based on its strong performance and growth prospects,

Motilal Oswal analysts project a 10 per cent volume growth and a compound

annual growth rate (CAGR) of 15 per cent, 16 per cent, and 18 per cent in

revenue, EBITDA, and profit after tax (PAT), respectively, over financial year

2024-2026 (FY24-26).

Considering

these factors, analysts reiterate a ‘buy’ rating, with a revised target price

of Rs 1,600, underlining the company’s potential to exceed its cargo volume

guidance for FY24.