Office Address

123/A, Miranda City Likaoli Prikano, Dope

Phone Number

+0989 7876 9865 9

+(090) 8765 86543 85

Email Address

info@example.com

example.mail@hum.com

123/A, Miranda City Likaoli Prikano, Dope

+0989 7876 9865 9

+(090) 8765 86543 85

info@example.com

example.mail@hum.com

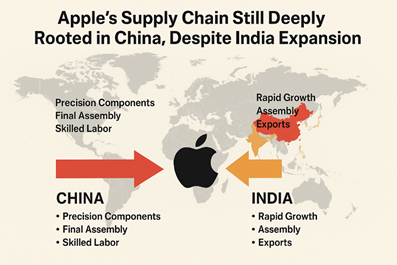

Despite a visible pivot to reduce dependence on China,

recent data reveals that the world’s second-largest economy remains the hub of

Apple’s most complex and high-value operations. According to the American Enterprise Institute (AEI), China currently

houses around 50% of Apple’s electronics manufacturing facilities, a decrease

from the 60–70% share prior to 2018. While this marks progress toward

diversification, China remains dominant in final assembly and component

manufacturing, especially for high-tech inputs like lithium-ion batteries,

printed circuit boards, and precision mechanical components…Even amidst

escalating geopolitical tensions and a steep 54% U.S. tariff on Chinese goods

in 2025, Apple continues to rely heavily on China’s industrial backbone. The

country’s integration into the Apple ecosystem is not merely logistical but

structural—its role in Apple’s

manufacturing is foundational. China is

not just a supply-side partner; it is a key market for Apple’s products. In

the December 2024 quarter, Greater China accounted for 17% of Apple’s global

revenue, underlining the strategic importance of maintaining strong

manufacturing and commercial ties with the region…Notably, about 37% of Apple’s 35 suppliers in Vietnam are either

Chinese or Hong Kong-based, illustrating how Apple’s international footprint is

still deeply anchored to Chinese expertise. Apple’s supply chain expansion into

India is real and growing fast. In the fiscal year ending March 2025, Apple

assembled $22 billion worth of iPhones in India—a 60% year-on-year increase.

India now produces approximately 14% of global iPhone output, up from just 3.1%

in 2021. During the same period, India exported $17.4 billion worth of iPhones,

highlighting its emergence as a key node in Apple’s global network. Apple and

its suppliers are aiming high: by 2026–27, they plan to produce 32% of the

world’s iPhones in India, with a production value reaching $34 billion…Despite Apple’s

diversification strategy, full decoupling from China is years away, if not

longer. The reasons are structural: Scale: China’s ecosystem supports hundreds of

thousands of workers; Foxconn’s Shenzhen complex alone employed over 500,000

workers in 2010. Infrastructure: China’s supply chain infrastructure, from rail

freight to port access, is deeply optimized for high-volume electronics

production. Automation & Quality Control: Apple’s strict quality standards

are harder to maintain in India, where recurring quality issues have already

impacted iPhone 16 production.

Even tariff policies don’t fully incentivize a shift. While the U.S. has imposed tariffs of 54% on China

and 26% on India, other countries like Vietnam face 46% tariffs, complicating a

complete transition of production from China to alternative markets.

Apple’s

diversification to India is both strategic and substantial, with iPhone output

growing significantly and export numbers rising sharply. But the data tells a

clear story: China remains the nerve center of Apple’s global supply chain,

especially in high-value, precision-driven manufacturing.

India’s rise in Apple’s ecosystem is promising, but

current limitations around quality, infrastructure, and self-sufficiency

suggest that China’s dominance will persist in the foreseeable future. For Apple, the path forward will be less about

decoupling and more about strategic hedging, balancing political risk, tariff

exposure, and operational efficiency across a multi-country supply chain that

still, unmistakably, leans on China.